Geopolitical Tensions: Understanding Market Impact During Times of Conflict

Global attention has turned to escalating tensions between Israel and Iran, creating ripples of uncertainty across financial markets worldwide. Following Israeli military actions targeting Iranian nuclear and military installations that commenced on June 13, swift retaliatory measures followed. Though the landscape remains fluid and subject to rapid change, emerging reports suggest Iran may consider ceasing hostilities and returning to nuclear program negotiations. This development unfolds against the backdrop of ongoing warfare in Gaza and various regional conflicts across the globe.

While humanitarian impacts remain the paramount concern, investors must also comprehend how such developments affect market dynamics. A primary worry among market participants centers on whether these incidents might spiral into comprehensive global warfare. Although such escalation remains within the realm of possibility, recent historical precedent suggests otherwise. Major conflicts, including Russia’s Ukrainian invasion and Hamas’s assault on Israel, have generally remained geographically contained, resulting primarily in temporary equity market fluctuations.

This observation doesn’t minimize the gravity of these conflicts, but rather emphasizes that portfolio overreactions to such events often prove unproductive. During these periods, maintaining perspective becomes crucial, alongside focusing on historical lessons and enduring market patterns. What elements should investors prioritize to maintain discipline amid current market conditions?

Regional tensions have intensified significantly

Recent developments represent a notable escalation in Israel-Iran relations. Israeli military operations have focused on Iranian nuclear installations and military command structures, with intelligence suggesting significant damage to uranium processing capabilities. Iran’s response has included missile and drone strikes, with several reaching Israeli territory. The confrontation has also compromised essential infrastructure for both nations, affecting natural gas installations and petroleum refineries.

At the risk of oversimplification, historians typically approach each event as distinct, possessing unique narratives, origins, and outcomes. Economists, conversely, seek patterns and commonalities across events to formulate broader insights. For investors, both viewpoints prove valuable in determining which lessons apply to current circumstances. As the familiar adage suggests, while history may not repeat exactly, it frequently echoes similar themes.

The included chart offers historical context regarding geopolitical developments spanning the last quarter-century. This encompasses Middle Eastern conflicts that influenced petroleum prices, such as Iran’s 2019 drone attacks on Saudi Arabian facilities. These episodes demonstrate that although short-term market fluctuations can occur, markets have generally rebounded from geopolitical disruptions, often within weeks or months following initial events. During these intervals, underlying economic cycle trends proved more significant determinants.

Energy prices have experienced significant fluctuation

In immediate terms, petroleum prices serve as a conduit through which regional conflicts influence global markets. Initial market responses to recent tensions concentrated on energy sectors, with Brent crude futures climbing beyond $74 per barrel. While energy prices remain unstable, they retreated toward $70 per barrel amid potential de-escalation prospects.

Energy costs impact worldwide economic activity as they constitute substantial inputs across all goods and services. Elevated petroleum prices translate to higher gasoline and transport expenses, increasing costs for consumers and enterprises alike. This effect amplifies through potential disruptions to vital shipping corridors, particularly the Strait of Hormuz in the Persian Gulf. This waterway represents a crucial passage for roughly one-third of global oil transportation.

Nevertheless, maintaining perspective on current energy price levels remains essential. While recent fluctuations are noteworthy, prices stay considerably below 2022 peaks during early Russia-Ukraine conflict stages, when oil surpassed $120 per barrel. Present levels around $70 fall within ranges experienced throughout recent years. This year alone has witnessed petroleum price variations between $60 and $82 per barrel.

Additionally, the United States has achieved greater energy independence over two decades. American petroleum production currently exceeds 13.5 million barrels daily. Many might find it surprising that America leads global production in both oil and natural gas. While the U.S. continues requiring foreign petroleum and remains sensitive to international pricing, substantial domestic supply helps shield the American economy and financial markets.

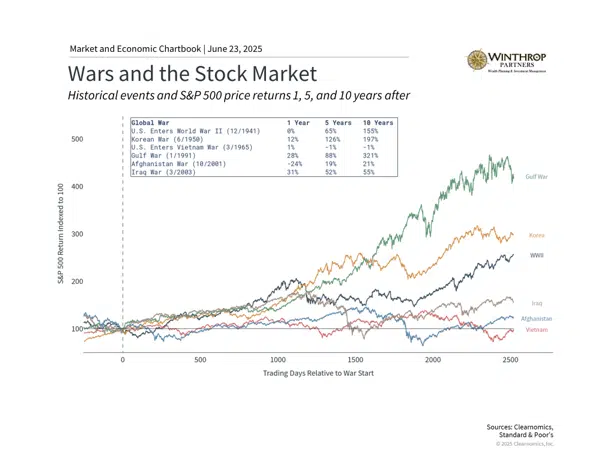

Conflict effects on investment portfolios correlate with economic cycles

For investors concerned about expanding global conflicts, broadening perspective can provide valuable context. From World War II through the Iraq War, markets may have responded to these conflicts short-term, but long-term performance was determined by fundamental investment factors.

For instance, World War II catalyzed industrial production following the Great Depression and created substantial workforce shifts as women entered employment. These elements helped drive economic growth throughout the remaining century. Similarly, the Gulf War influenced petroleum prices but also coincided with the 1990s Information Technology boom. Conversely, the post-Vietnam War decade aligned with elevated energy costs and stagflation, producing disappointing market results.

Again, this analysis doesn’t diminish the humanitarian and social consequences of warfare. Regarding current circumstances, outcomes will largely depend on whether conflicts expand or begin de-escalating. Major power involvement and threats to essential supply chains add complexity, yet history indicates that even substantial regional conflicts typically exert limited long-term influence on global financial markets.

The bottom line? Although Middle Eastern tensions have generated temporary market volatility, investors should preserve perspective and resist overreacting to news headlines. Maintaining a portfolio aligned with long-term financial objectives remains the optimal strategy for navigating geopolitical uncertainty periods.

Winthrop Partners is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training. The information provided is for informational purposes only and should not be considered investment, legal, or tax advice. All investments carry risks, including the possible loss of principal. No advice or recommendations are being provided in this advertisement, and you should consult a qualified professional before making any financial decisions. Past performance is not indicative of future results.

Thomas Bunting is a Financial Advisor at Winthrop Partners. He has more than 50 years of experience in accounting, financial planning, and tax planning. Prior to joining Winthrop Partners, Tom held the roles of partner, managing partner, and senior partner with a mid-sized CPA firm that provided a full range of accounting, tax and financial planning services.

Tom is a member of the American Institute of Certified Public Accountants, the Personal Financial Planning and tax sections of the American Institute of Certified Accountants, and the Pennsylvania Institute of Certified Public Accountants. He was also a former member of the AICPA governing council and a past president of the PICPA. He earned his BS in Accounting from Temple University.