Strategies for Building Inflation-Resistant Investment Portfolios

Natural disasters come in many forms – some strike suddenly like earthquakes, while others gradually wear away foundations like erosion. Both require thoughtful preparation and protective strategies. Financial challenges follow a similar pattern, where the most significant threats to wealth aren’t always immediate crises but can unfold slowly over decades. Inflation represents both types of risk, presenting investors with sudden price spikes and the steady decline of purchasing power that impacts markets today.

Investors familiar with the inflationary periods of the 1970s and early 1980s, or the recent price increases following the pandemic, recognize this dynamic. While inflation remains more persistent than many anticipated, and concerns exist that tariffs could drive consumer prices higher, current inflation coincides with robust employment levels, strong consumer spending, and solid corporate earnings. This creates a nuanced landscape for investors and policymakers who must navigate the balance between economic growth and price stability.

Instead of reacting to inflation after it becomes problematic, prudent long-term investors should construct portfolios capable of weathering various economic scenarios while maintaining focus on their financial objectives. What insights do current inflation data provide about the economy and investment strategies?

The gradual decline of purchasing power through inflation

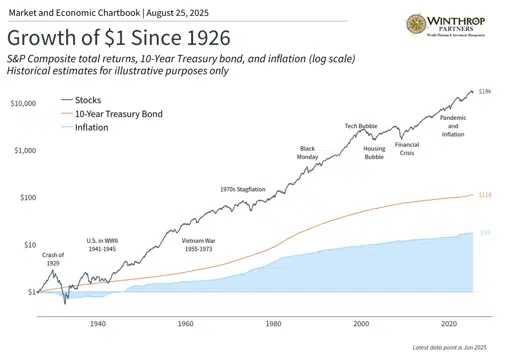

The fundamental purpose of investing for most people involves outpacing inflation to preserve and grow their wealth. Whether through stocks, bonds, certificates of deposit, or alternative investments, maintaining purchasing power ensures future financial security and lifestyle goals remain achievable. The accompanying chart demonstrates this reality starkly. Items that cost $1 one hundred years ago now require $18. The data also reveals how price pressures intensified during the 1970s and have accelerated again in recent years.

This perspective might suggest that zero inflation or even deflation would benefit consumers. However, inflation affects more than individual purchasing decisions – it reflects overall economic health. Contemporary economic theory supports maintaining low but positive inflation rates, typically around 2%, as optimal for both individuals and the broader economy.

Moderate inflation provides central banks flexibility in monetary policy implementation, encouraging spending and investment when economic conditions warrant such measures. Additionally, modest inflation helps avoid deflationary cycles, where declining prices cause consumers to postpone purchases expecting further price reductions.

Therefore, distinguishing between individual and economy-wide impacts proves essential. While 2-3% inflation historically supports healthy economic growth, even these moderate levels can harm savers significantly. Though these rates appear manageable compared to 1970s double-digit inflation or recent pandemic-related surges, their compounding effects accumulate substantially over time.

Consider that 3% annual inflation doubles costs approximately every 24 years. This means $100,000 in current purchasing power would require $200,000 within two decades – a timeframe covering typical retirement periods. This erosion particularly challenges retirees and cash holders. For all investors, inflation establishes a benchmark that investment returns must exceed to build real wealth.

Current inflation remains persistently elevated

Regarding today’s inflationary climate, many worry about the sudden impact tariffs might have on price levels. Recent Producer Price Index data illustrates these concerns, showing business-level prices jumped significantly in July. Wholesale prices surged 0.9%, marking the largest monthly increase since June 2022 and exceeding economist expectations. Goods prices climbed 0.7% while services prices jumped 1.1% in a single month.1

These figures matter because wholesale price increases typically translate to consumer prices with several months’ delay as inflation moves through supply chains. This pattern suggests companies have absorbed tariff costs initially but may now begin transferring higher prices to customers.

The most recent Consumer Price Index data shows less dramatic increases but confirms inflation’s persistent nature. Latest figures indicate prices rose 2.7% annually for overall inflation, or 3.1% excluding food and energy prices which remained flat or declined. Housing costs drove much of this increase.2

Beyond economic abstractions, these numbers directly affect household budgets. Price increases appear in areas consumers notice most: restaurant meals increased 3.9% annually, medical care rose 3.5%, and auto insurance jumped 5.3%. Even furniture prices climbed 3.4%, adding pressure to family budgets already strained by years of elevated costs.

Strategic asset allocation essential for inflation protection

While these increases are significant, current inflation remains well below the double-digit rates experienced from 2021 to 2022. Nevertheless, even if tariffs don’t trigger sudden inflation spikes, they may elevate average price levels over time, diminishing cash value. This becomes particularly problematic when wage growth lags price increases and investors lack long-term allocations capable of exceeding inflation rates.

Understanding inflation’s portfolio implications proves crucial. The accompanying chart reveals that average cash interest rates have failed to match inflation over time. Additionally, money market fund holdings remain at record highs of $7.1 trillion despite declining short-term interest rates.3

While past performance doesn’t guarantee future results, historical data shows both stocks and bonds have exceeded inflation over extended periods, as the first chart illustrates. However, stocks can experience volatility during inflationary periods, as 2022 demonstrated. This highlights why balanced asset class exposure that can withstand both inflation and market volatility helps investors maintain progress toward their goals.

Most critically, investors should avoid making drastic portfolio adjustments based on monthly inflation reports or tariff concerns. While positioning portfolios for various scenarios remains important, overreacting to short-term data often results in poor timing decisions that undermine long-term financial objectives.

The bottom line? Inflation’s steady erosion of purchasing power represents a fundamental investment challenge. Maintaining a well-balanced portfolio designed to generate both income and growth offers the most effective path to achieving financial objectives.

As a Chartered Financial Consultant at Winthrop Partners, Jennifer works closely with clients

and advisors in all areas of the financial planning process. On a daily basis, her key role is the

operations of the firm. With over 29 years of experience, she prides herself with providing

clients with a consistent high-quality experience when doing business with Winthrop Partners.